When do we not think about taxes? Whether we’re making investments, contemplating a major purchase, estate planning, or closing out the calendar year, taxes are always top of mind.

In recent years, Certificates of Deposit (CDs) have regained popularity due to their low risk and relatively high returns. Even as interest rates trend downward, many financial institutions still offer competitive CD rates, making them an attractive option for savers. But while you focus on locking in strong yields, there’s one key factor you may have overlooked – taxes.

Here’s what you should know about how your CDs could impact your tax filing:

Do You Pay Taxes on CD Interest?

All types of income you earn in a taxable year must be reported to the IRS. That includes the interest on your CDs. Keep in mind, as you earn interest on your CD even before it is fully matured, it is still considered taxable income and subject to annual federal income tax.

When are taxes due on a CD?

Depending on if the CD is a short-term or long-term CD, the due dates are as follows:

- Short-Term: Interest earned on CDs with terms of one year or less is considered taxable income in the year that the CD interest is paid out. For example, if you opened a 6-month CD in August 2024, and the interest didn’t pay out until the CD maturity in February 2025, the interest is taxed in 2025. Note: Many financial Institutions pay interest each month or quarter even on short-term CDs.

- Long-Term: CDs with terms over a year are taxed as interest is earned and paid over the CD term. Interest is considered taxable income in the year that you are legally entitled to it. This means that the interest that is paid to you either as credit to the CD or paid to you in another method such as a check is taxable in the year it was earned. Interest that is still accruing but not paid isn’t taxed until it is paid to you. For example, if you have a CD with a term of five years, and the interest is credited quarterly to the CD, you will owe tax on the interest paid in each of the quarters during each year that you hold the CD before maturity.

How Are CDs Taxed?

CD interest falls in the category of taxable income (salary, wages, tips, severance pay, overtime, bonuses, unemployment, etc.) and is taxed at the same rate. You can calculate the amount you owe on your CD interest based on your tax bracket and the dollar amount you gained in CD interest.

However, you do not have to claim interest that is accruing but not yet paid to you or the CD. If interest compounds daily – interest paid on the deposited amount plus interest each day but paid to the CD every quarter on the anniversary date of opening — then the CD could have interest that is accrued at year-end but has not been paid to the CD yet.

For example, if a CD is opened on August 5, 2024, interest would be paid on November 5, 2024. The interest that is accruing from November 6, 2024, through year-end is not reportable for the tax year of 2024 as it has not been paid to the account yet.

Many banks pay interest monthly or quarterly on the calendar month, and some pay monthly or quarterly on the anniversary date of the CD open date, so it is important you clarify with your financial institution when they pay interest on your account.

Do I report my principal and interest when I cash out my CD?

Only interest you earn on your principal amount is taxed. Financial institutions will report the interest you earned to the IRS and will provide you with a Form 1099-INT where you will need to claim the amount you earned as interest. You are not responsible for paying taxes at the time you “cash out” but are responsible for paying the taxes in the year that the interest was paid to you. For example, if your CD has a principal balance of $20,000 and you earned $500 in total interest for the entire CD term at the time you cash out the CD, you will only be taxed for interest that was paid to you in the current calendar year.

How to Report CD Interest on Your Tax Return?

When you’ve earned at least $10 in CD interest for the year, financial institutions are required by law to report this information to the IRS and will provide you with Form 1099-INT by January 31 for your tax records. If you have multiple CD accounts, you will receive a copy of Form 1099-INT for each account. When filing your tax return, report this interest on Form 1040 Line 2.

Is CD Interest Taxable Before Maturity?

Yes, CD interest is taxable in the year it is credited to your account, not just at maturity. This means you must report interest earned annually, even if you don’t withdraw it. For example, if you have a 5-year CD that has interest credited to the CD or is paid directly to you annually, you need to report and pay taxes on interest each year. Understanding this helps in planning accurate tax payments and avoiding surprises during tax filings.

What if I pay an early withdrawal penalty? How does this affect the taxes I pay on my CD interest?

Your bank will charge you an early withdrawal penalty fee when you withdraw funds from your CD before it reaches the maturity date – the end of its term. Typically, you are only charged the early withdrawal penalty on the funds withdrawn, not on the full CD amount. If you do incur an early withdrawal penalty, you can deduct the amount of your early withdrawal fee on your tax return, which will offset how much you pay in taxes on the interest you earned on your CD.

For example, if you earned $100 in interest, you would pay taxes on that $100. But if you pay an early withdrawal penalty of $20, you can deduct that from the interest you earned, leaving you to pay tax on $80 of income.

But There Are Exceptions to When You Pay Taxes on CD Interest…

You can defer paying taxes on your CD interest in a couple of ways. When a CD is placed in tax-advantaged accounts such as a tax-deferred IRA and 401(k), you are not taxed on your interest until you withdraw your total earnings, typically around retirement. On a Roth IRA CD, the interest is tax-free if you hold your first Roth IRA for 5 years and are 59.5 years old or older. With a traditional IRA CD, the interest does not have to be claimed until you withdraw the funds after age 59.5 years old or older. You typically are in a lower tax bracket, and you may get the extra benefit of being able to deduct the contribution too.

Another option is opening a short-term CD. This provides the option to defer taxes from one year to the next. By investing in a short-term CD in one year with a maturity date in early January of the next year—i.e., before the January 15 due date for the final estimated tax payment for the prior year—a taxpayer can enjoy both a better interest rate and one-year tax deferral on the CD interest.

Note: If you exercise any of the IRA CD options it is important to remember that your annual contribution to IRA accounts remains below the contribution limits set by the IRS. For 2025, the combined Traditional and Roth IRA contribution limit is $7,000. If you are 50 or older, the limit is $8000, However, income limitations also apply to ROTH IRAs.

How can I use CDs to prepare for paying my taxes?

One common use for a CD is saving for near-term planned expenses, like tax payments or tuition. This makes CDs often a highly effective way of managing funds that you do not expect to need for a matter of months or years, but you do not want to place yourself at risk of losing your principal by investing in stocks or other assets that are subject to price volatility. And for an extra layer of security, CDs are protected – up to a minimum of $250,000 per depositor – under insurance provided by FDIC or NCUA.

Final Takeaway

Before you open your next CD, consider the earnings you will make and when you will be expected to pay federal income taxes on them. This may influence the maturity you select.

Disclaimer: This is not intended as tax or legal advice. Please consult your tax advisor or financial planner to understand how these topics may affect your individual financial situation.

Read More

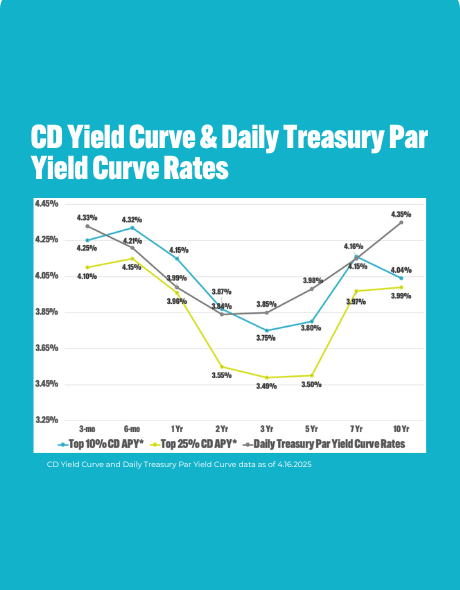

How the Current Economic Landscape Affects the Yield Curve—and CD Rates